To ensure lnternal Rating Based (IRB) models are adequately addressing regulatory requirements, IRB models are subject to a regular validation cycle, with emphasis given to a thorough model backtesting and benchmarking. All validations require testing of conceptual soundness which typically uses additional information obtained from Model monitoring. In addition, benchmarking to external data and set-up of challenger Models often provides additional insights into the adequacy of Models.

Credit Models used for IRB Basel and IFRS 9 requirements deteriorate when economic condtions or business strategies undergo significant change. A case in point is a deteriorating Model performance due to failure of capture emerging risks. Consequently, both Basel IV and IFRS 9 raised the standards expected for Model validations by regulators and accountancy standards alike. Demonstrating robustness of Credit Models under stress and ensuring accurate Model calibrations are in place, are deemed a pre-condition for efficient capital and IFRS9 calculations. Click the links below and read about details of Credit Validations and how Auriscon can support:

→ The Elements of Credit Risk Validation (selected examples)

Disclaimer: Data, charts and commentary displayed herein are for information purposes only and do not provide any consulting advice. No information provided in this documentation shall give rise to any liability of Auriscon HK Ltd and Auriscon Ltd.

Our Aproach

is to support or independently carry out validation activities, both according to the timetable of the institutions validation framework or ad-hoc based on requirements of the moment and circumstances. We assist in defining and performing statistical testing and analysis covering validation of Basel and IFRS9 risk parameter PD, LGD, EAD and effectiveness of monitoring systems.

Planning & Objectives

We support validations covering, but not limited to, Data Quality and Integrity, Statistical Testing, Conceptual Soundness, and Benchmarking. We support in devising validation frameworks and in automating validation testing and report generation based on the R programming language.

Specialisation

As a specialist provider with expertise in Credit and Model Risk, we can suport based on a tailored approach suitable for Credit Wholesale and Retail portfolios.

Risk-Based Approach to Validation Testing

Identifying latent and emerging Risks is a key aspect every validation should aim to capture. With our support, additional view points on prevailing credit and economic positions are added. With a thorough statistical testing applied, suitably underpinned by benchmarking and backtesting, information is gather critical information about Model performance and Model risk transparently.

Contact us to request further details on our support.

→ Contact

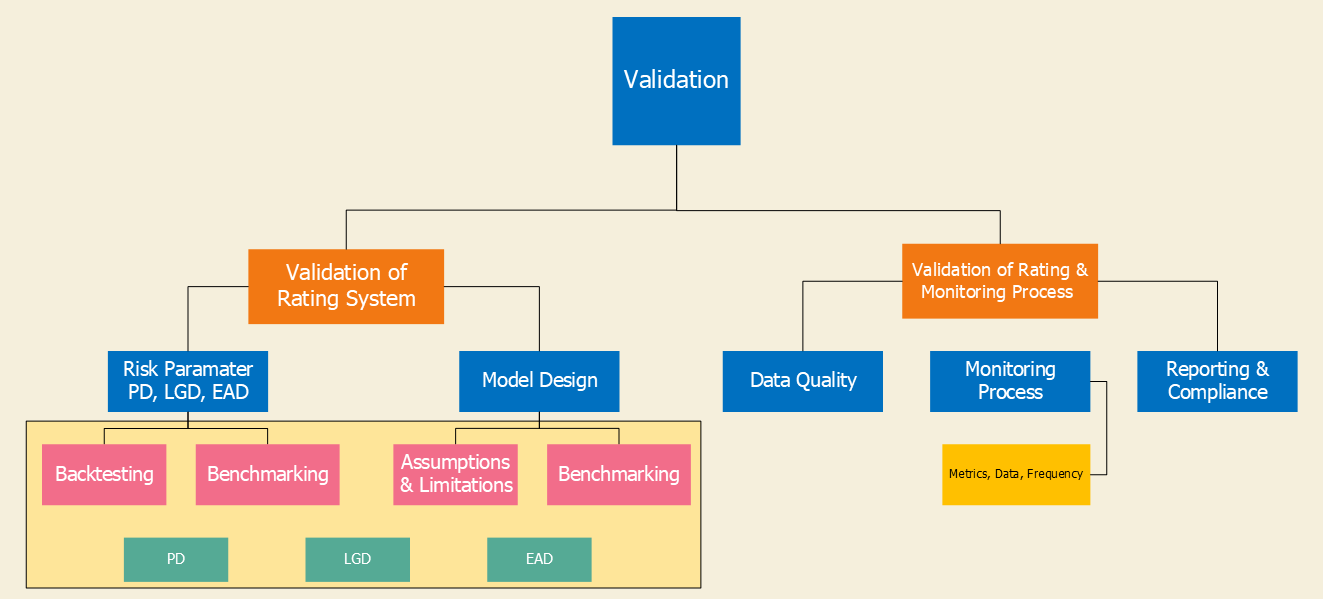

Validation Levels and Elements

Elements of PD Validation (example)

- Statistical Calibration Testing

- Backtesting and Benchmarking

- Number of Overrides

- Discriminatory Power

- Portfolio Stability

- Challenger Models

Validation Levels

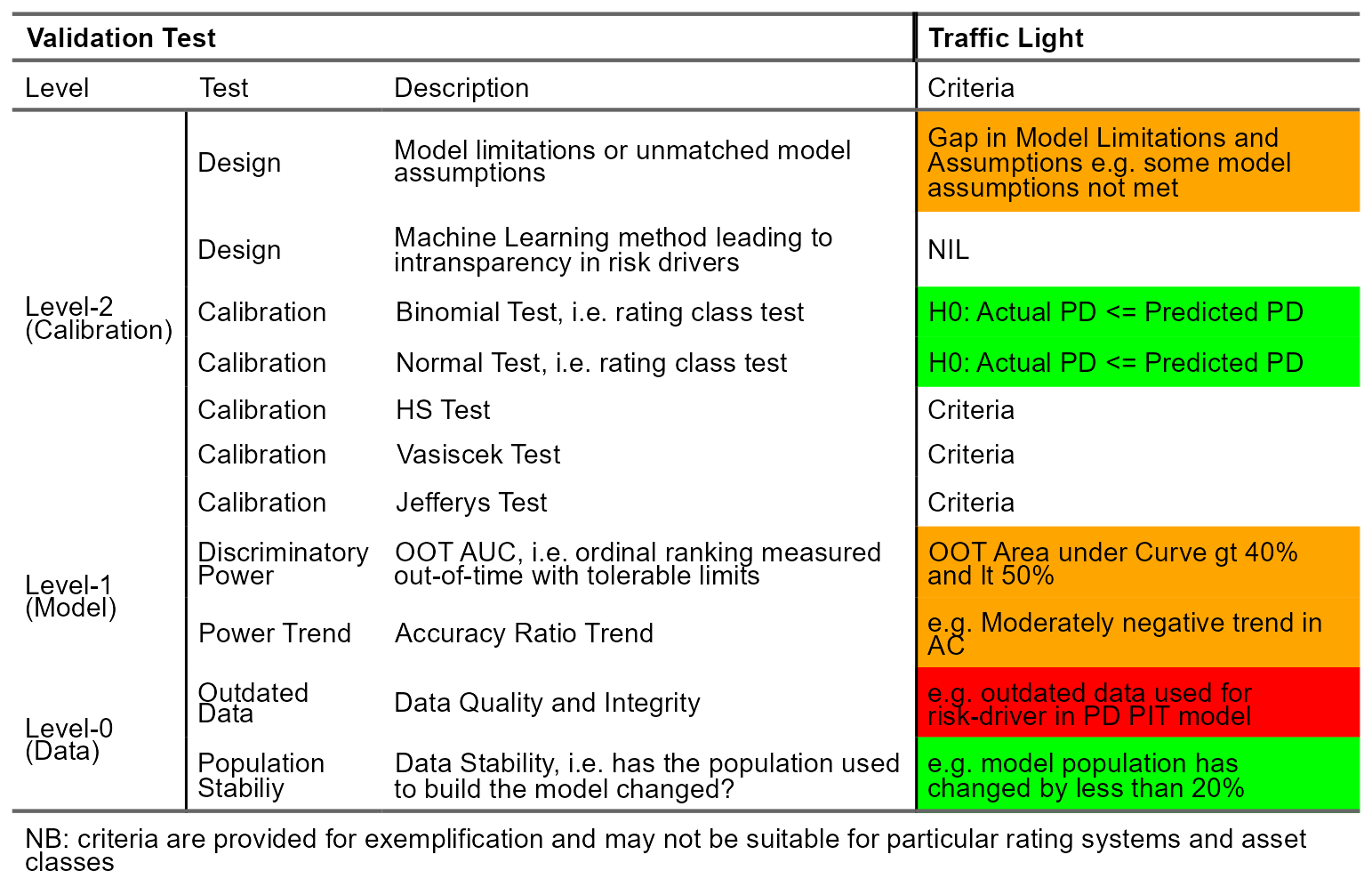

Validation Testing proceeds from Data (Level 1) to Model (Level 2) to Calibration Level (Level 3). Different validation tests are performed and assigned as illustrated in the table shown below:

The Elements of Validation

The following few sections display elements of validations illustrated for a PD Model.

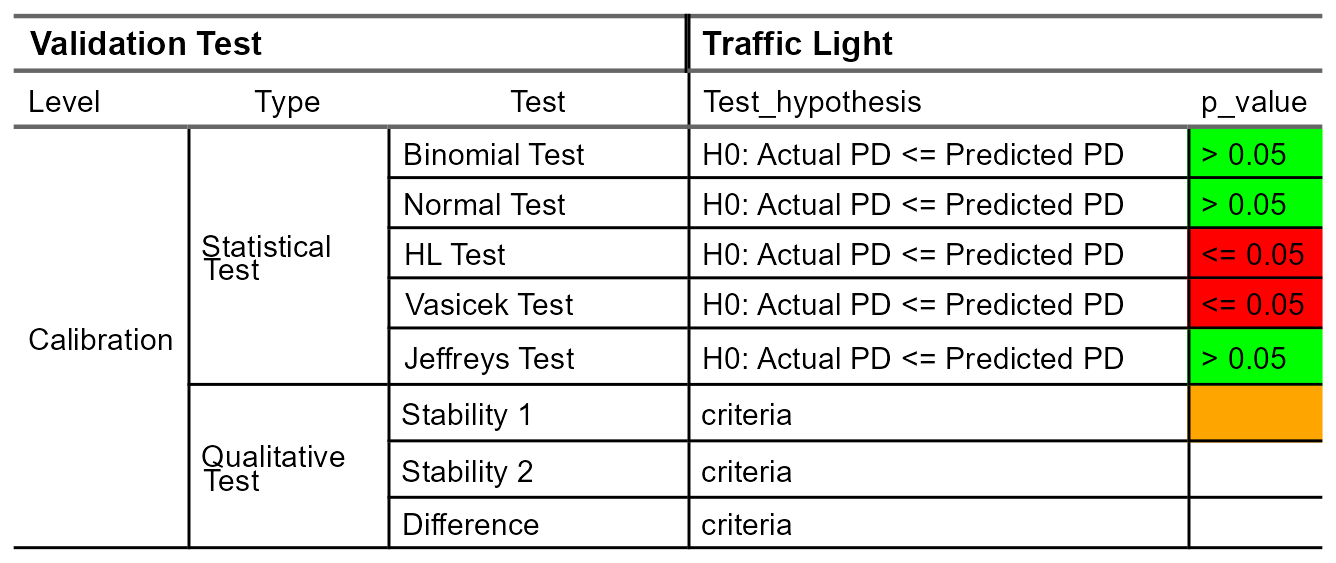

Validation Testing at Calibration Level

Traffic-Light-Dashboard Level 2

Level-2 for PD (example)

Traffic-Light indications for calibration accuracy

Validation Testing at Model Level

Traffic-Light-Dashboard Level 1

Conceptual soundness and Model assumptions.

Limitations pertaining to the Model.

Discriminatory power of a rating (scoring) Model.

Variable selection process and plausibility thereof.

Overrides frequency and strength for indicator of deteriorating performance.

Validation Testing at Data Level

Level 0

- Data Quality, e.g. metrics such as Currentness of Data should be integrated into validation testing at Level-0..

- Representativeness of data and data stability of the portfolio's obligor population in terms of characteristics can be tested using metrics suchs as Population Stabiliy Index, t-test, histogram and percentiles.

- Integrity of data, i.e. is the credibiliy of data sources confirmed?