We support in Credit Risk Analytics specializing in the development and validation of Credit Risk models. At Auriscon we draw on multiple model building techniques to ensure our customers obtain specialized support for model applications and uses in IRB, Portfolio Credit Risk, Stress Testing and IFRS9. Through our capacity to deliver end-to-end we support teams and institutions in conceptualizing, model building, model testing, prototypical coding, model risk review and technical documentation.

At Auriscon, we have suitable expertise to enable knowledge transfer based on in depth industry practice. For further details, feel invited to browse through an outline of supported activities displayed below. For inquiries on support towards a succesful project outcome contact us.

→ Contact

Disclaimer: Data, charts and commentary displayed herein are for information purposes only and do not provide any consulting advice. No information provided in this documentation shall give rise to any liability of Auriscon HK Ltd and Auriscon Ltd.

Our Approach

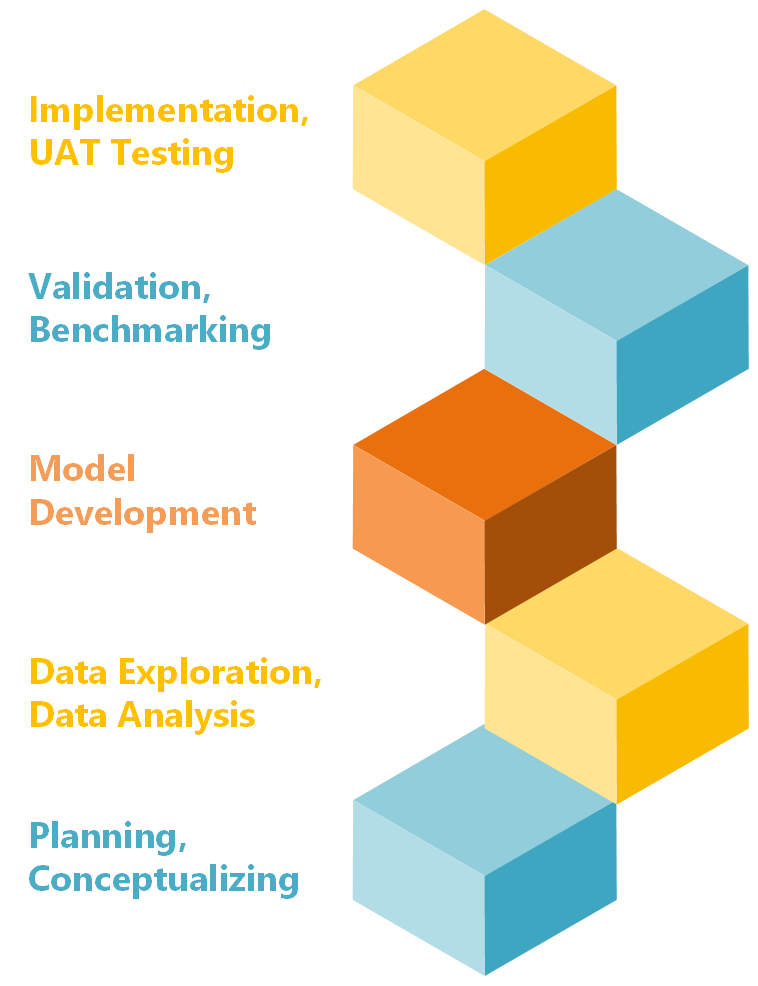

We involve our clients throughout the model development and validation process, beginning from the initial concept proposal and an agreed terms of reference through to the final implementation phase. Team member of Auriscon Limited have the right expertise. We can support on-site or by working remotely based on flexible allocations.

- We confidentially deal with methodological concepts and analytical models.

- We draw on business insights to deliver tailored solutions.

- We advise on industry standards and point to emerging risks.

- Through our advising on methodology solutions and with our supporting in developing / validating credit risk models our clients can successfully manoeuvre a challenging regulatory and market environments.

Our Services in Credit Analytics

SCORING, IFRS-9 and BASEL RISK PARAMETER - DEVELOPMENT & VALIDATION

Development and Validation of Credit Risk Models, covering Application Scoring, IFRS9 ECL and Basel parameter estimation for PD, LGD and EAD Models.

BOOSTING CREDIT RISK MODEL PERFORMANCE

Evaluation and enhancement of credit model performance. Profitability driven Credit Analytics, to enable enhancing Credit Models through accounting for Profitability aspects and measures.

EVALUATING CREDIT PORTFOLIO RISK

Relying on Credit Portfolio Risk Models should be supported by insightful analytics, tools and data integrity. Auriscon supports in delivering exactly this. IFRS 9 Expected Credit Loss ECL, Economic Capital Models, Risk-adjusted performance for Credit Lending.

- Credit Loss Distributions.

- Segmentation of customer groups.

- Credit Portfolio Vulnerabilities.

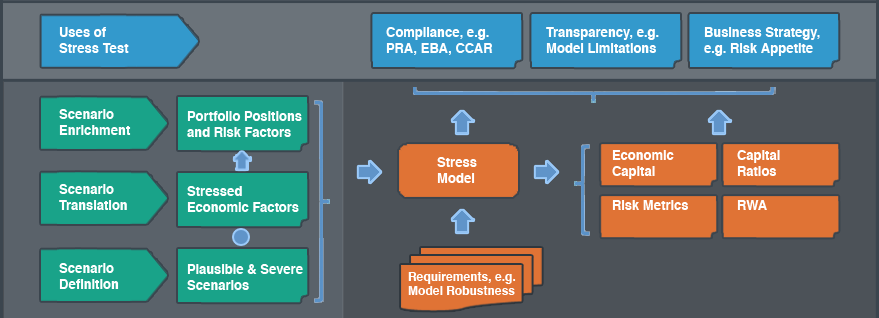

STRESS TESTING

Model concepts and developments covering Scenario Planning, Factor Identification, and Economic Response based on modern methods e.g. Vector Autoregression.

MODEL RISK REVIEW

Review of Model concepts and developments incuding validations, regulatory compliance and model governance. Our support in reviewing model risk and compliance renders a suitable add-on insight.

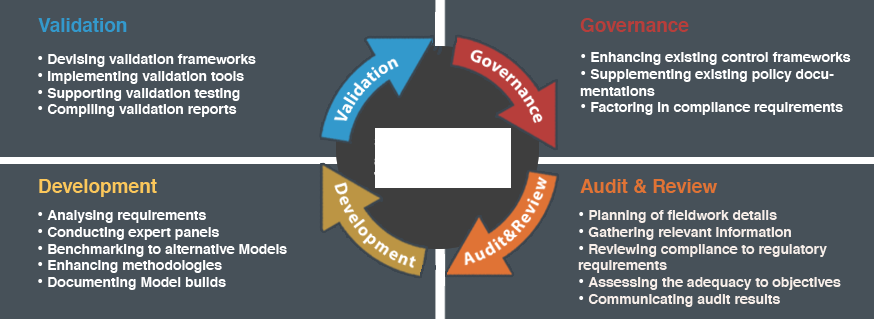

Illustration of Consulting Support:

At Auriscon we can support on-site or by working remotely based on flexible allocations. We collaborate effectively with functional teams and stakeholders to assist in attaining the project goal. A few examples of how Auriscon can support your model development or validation projects are shown below for illustration.

OBJECTIVE

HOW

Boosting of PD / LGD Models in terms of performance and positive mpact on profitability.

- Alternative Data Sources to accommodate new significant credit drivers.

- Feature Engineering to identify better predictors.

- Profitability aspects.

- ML methods integared in Modelling and Models.

Example: Model Benchmarking

| Interpretabiliy | Accuracy | |

| Regression (logistic) | Good | Medium |

| Decision Tree | Very Good | Good |

| Boosted Tree | Poor | Very Good |

| Deep Learning | Poor | Very Good |

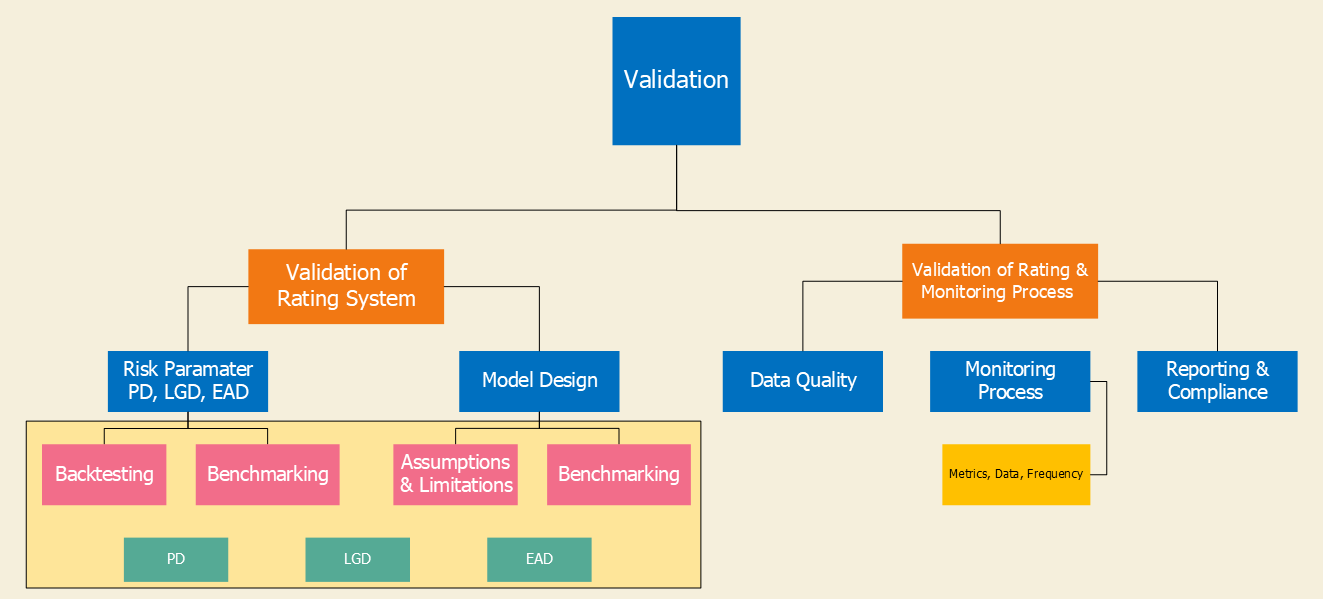

Validating IRB, IFRS9 and Scoring Models

Support on cyclical of PD, LGD, EAD Model validations.

Validation testing of Credit Model predictions (backtesting), performance and stability.

Benchmarking to challenger models.

Feedback on identified gaps in Model monitoring and on shortfalls to Regulatory expectations.

Identifying and quantifiying model risk related to root causes in model design, data, validation gaps, etc.

Elaborating on process ineffeciencies to match risk mitigation solutions to root causes.

Communicating review outcome and writing report on model risk review for internal use.

Detecting

- Model design limitations.

- Data limitations

- Calibration bias leading to alert on inadequate model outputs.

- Shortcomings in validations e.g. identifying overlooked themes and details.

- Gaps in compliance to regulatory requirements e.g. Credit Risk (SS 11/13), Capital & Stress Testing (SS 3/18).

→ BACK

Development and conceptual planning for Scenario Planning, Factor Identification, Economic Response based on modern methods.

Demo for example on VAR:

Estimating & Calibrating

- Economic Response Model using Macro linkages.

- Data Selection

- Scenario Selection.